English

English  Vietnamese

Vietnamese

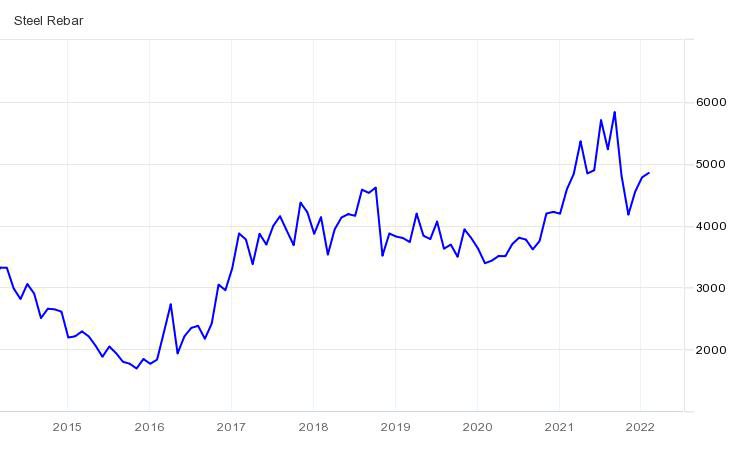

China's steel prices experienced an unpredictable 2021 when the Beijing government asked enterprises to cut steel production to lower greenhouse gas emissions.

In 2022, the market generally expects that the steel price will be less volatile because the Chinese government is likely not to control the steel industry as strongly as last year.

Sharing with S&P Global Platts, industry experts predict that China's crude steel output will increase in the first half of the year and then cool down in the second half. However, the output for the whole year remains the same as in 2021.

In addition, steel prices are also expected to be less volatile, but the full-year average price may decrease a bit due to slow growth in overall demand.

S&P Global Platts found that last year, hot-rolled (HRC) steel prices on the spot market in Shanghai fluctuated between 4,420 yuan and 6,680 yuan per tonne ($694-$1,050 per tonne). , the average price for the whole year is about 5,320 yuan/ton.

S&P Global Platts sources estimate that this year's price will be in the range of 4,000 - 5,500 yuan/ton.

Here are the key factors that could impact China's steel industry in 2022:

1. Steel demand of the real estate industry cools down

China's real estate sector is expected to continue to decline this year. The growth rate of this industry will slow down significantly after many years of receiving stimulus from the government, specifically in the period 2016 - 2020.

One obstacle for the real estate sector is that China's urbanization rate has reached 64% in 2020. Normally, urbanization will slow down and steel consumption will also go down when this rate comes. threshold 60%. Over the past 20 years, urbanization has been a key driver of the real estate industry and the country's steel demand.

The possibility of China's imposition of a property tax in the near future as well as a drop in the birth rate will also put pressure on real estate development in the long term, S&P Global Platts noted.

On the other hand, Beijing has begun to loosen monetary policy and financial restrictions on the real estate sector since late last year. This will support real estate, which can help investment in the real estate sector slow down from the second quarter. However, the government's efforts are not enough to reverse the quiet trend of the real estate industry.

2. The manufacturing sector still needs steel but there are risks ahead

For most of 2022, steel demand in the manufacturing sector is likely to be more stable than in the real estate sector. Some experts say the world's strong demand for Chinese goods is the main driver behind the steel demand outlook for the manufacturing sector.

However, it is almost certain that foreign demand for Chinese goods will decline in the second half of 2022. By then, global factory production will gradually return to normal, which will happen. at the same time as the tightening cycle of monetary policy in the US.

Elsewhere, some sources at S&P Global Platts are concerned that commodity demand in China may not yet recover. They said that it is difficult for Chinese household incomes to improve to promote consumption, so the demand for household appliances using steel has not been able to increase.

A steel production line in Anhui province, China. (Photo: Global Times).

3. Beijing's Environmental Policy

China has announced that industrial growth is a top priority in 2022, and relaxed requirements for cutting steel output in this year's emissions reduction policy.

Earlier this week, the Beijing government set 2030 as the new deadline for the steel industry to peak emissions, the previous target was 2025. Thereby, steel processing companies in China will have 5 more. more years to reach the CO2 peak.

Most steel mills, especially those in northern China, will operate at full capacity from January and will only start to lower output in the second half of the year. Normally, steel demand in the first 6 months is usually higher than in the last 6 months and the government is also "lighter" with the steel industry in the early part of the year.

In addition, China's gradual shift from traditional steelmaking technology to electric arc furnaces is also expected to make it easier for the polluting industry to meet its emissions targets.

4. Clear skies for the Winter Olympics

The Chinese government has asked steel mills in Hebei, Shanxi, Henan, Shandong and Tianjin provinces to keep crude steel output at 30% lower than the same period last year during the period. January 1 - March 15.

The purpose of the above policy is to reduce smog to ensure fresh air for the Winter Olympics to be held in Beijing from February 4 to 20.

Based on the same period in 2021, S&P Global Platts predicts that China's daily crude steel and iron production in the first two months of the year could reach 2.11 million tons and 2.59 million tons, respectively.

Starting in March, the steel production squeeze in northern China will gradually end. In parallel, the output of iron and steel may equal or exceed the level of 2021 in the first half of this year.

5. New iron and steel smelting capacity

Last year, China had a total new capacity of about 86 million tons of pig iron/year and 108 million tons of steel/year expected to come into operation, in the form of capacity swap with old facilities. However, S&P Global Platts estimates that by December of the same year, the new capacity will only come into operation at about 34 million tons of pig iron/year and 36 million tons of steel/year.

The commissioning of new iron and steel smelting capacity is expected to accelerate from the beginning of 2022. As some old mills have long been closed and new facilities are more efficient, the introduction of new capacity has come into operation. dynamics can help increase the overall power.

However, China's total iron and steel production capacity may gradually decrease from the end of 2022 or early 2023 as Beijing will tighten regulations on this capacity swap.

Vietnambiz

w300.jpg)