English

English  Vietnamese

Vietnamese

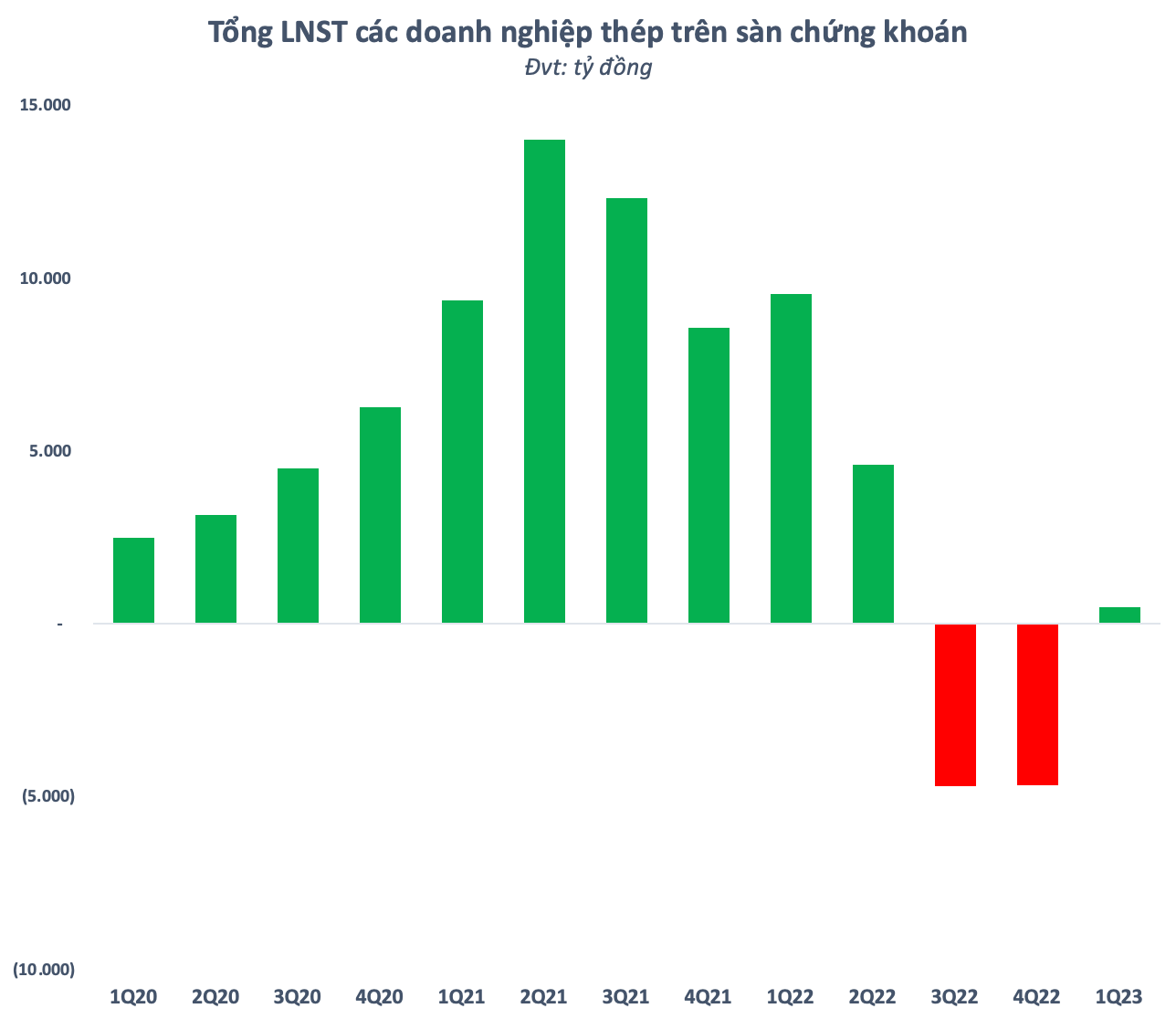

The business results picture of the steel industry has appeared bright spots after 2 consecutive quarters of decline. Tran Dinh Long, Chairman of the Board of Directors of Hoa Phat: "The most difficult period in the steel industry is over", the total profit of steel enterprises on the stock exchange is estimated at 500 billion dong in the first quarter. Although this number is still quite modest, it has improved significantly compared to negative 4,700 billion dong in the fourth quarter of 2022.

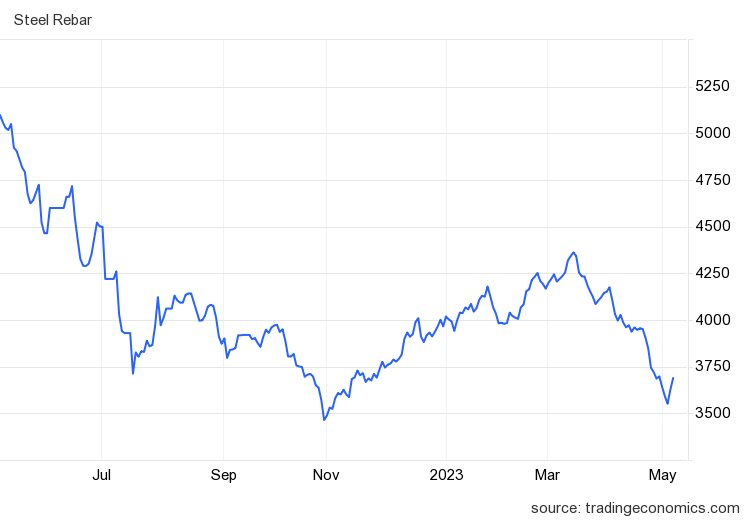

The profit recovery mainly came from the uptrend of steel prices in the first 3 months of the year. According to data from tradingeconomics, the price of rebar in the Chinese market in mid-March climbed to a nine-month high. Compared to the time of hitting a 2-year low at the end of October last year, the price of this commodity has increased by nearly 26%. However, steel prices then showed signs of reversal and began to decline sharply from the beginning of April until now. Domestically, prices of some steels are also at their lowest levels since the beginning of the year after many price adjustments.

Những gì khó khăn nhất đã ở lại phía sau?

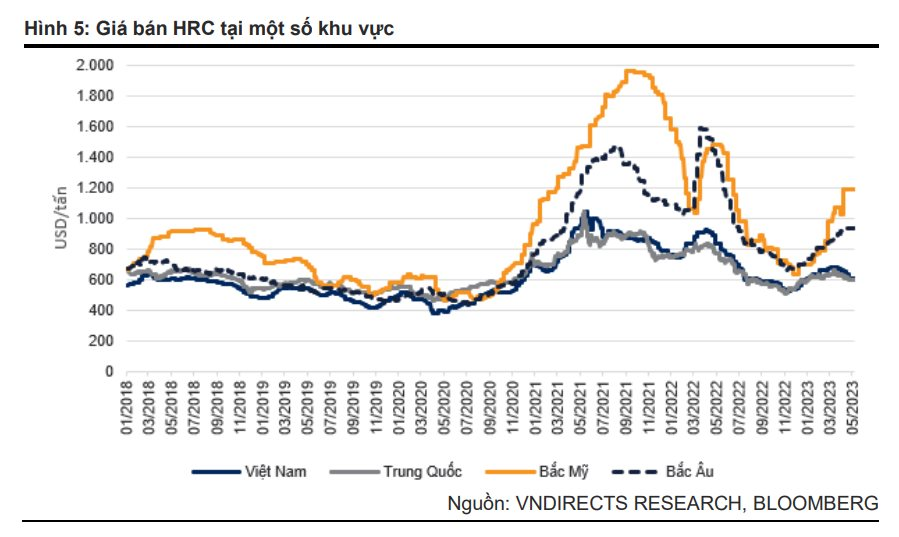

Trong báo cáo cập nhật ngành thép mới đây, Chứng khoán VNDirect nhận định giá bán thép HRC toàn cầu đã ghi nhận đà phục hồi đáng kể từ tháng 11/2022 sau khi Trung Quốc dỡ bỏ các lệnh giãn cách xã hội do Covid-19. Kỳ vọng nhu cầu thép tại Trung Quốc gia tăng đã khiến các nhà máy tích cực tăng hiệu suất vận hành và tích trữ nguyên vật liệu, dẫn đến việc giá đầu vào cũng tăng. Chi phí đẩy cũng là một tác nhân chính khiến giá bán thép bứt phá mạnh trong quý 1.

However, VNDirect pointed out that actual steel demand in China is not as strong as expected. The sharp increase in production output while weak demand has caused steel prices in China to decline since the end of March 2023.

Recently, the price of coking coal has continuously increased in the period January-March 2023 to the highest level since mid-2022, amid more optimistic forecasts for the Chinese economy and other major economies. . Coke prices are forecast to gradually decline in the long term and the biggest decline is expected in 2023 when supply (especially in Australia) improves and returns to normal levels.

VNDirect assesses that the lower selling price of output than input helps steel companies' EBITDA margin improve in April 2023. Therefore, the analyst team expects the gross profit margin of steel enterprises in the second quarter of 2023 to continue to improve compared to the previous quarter. However, steel demand will still be weak in the coming months, making profit margins of companies in the industry will still face many fluctuations, especially small companies with more limited inventory management skills.

Vietnam steel demand will recover strongly from 2024

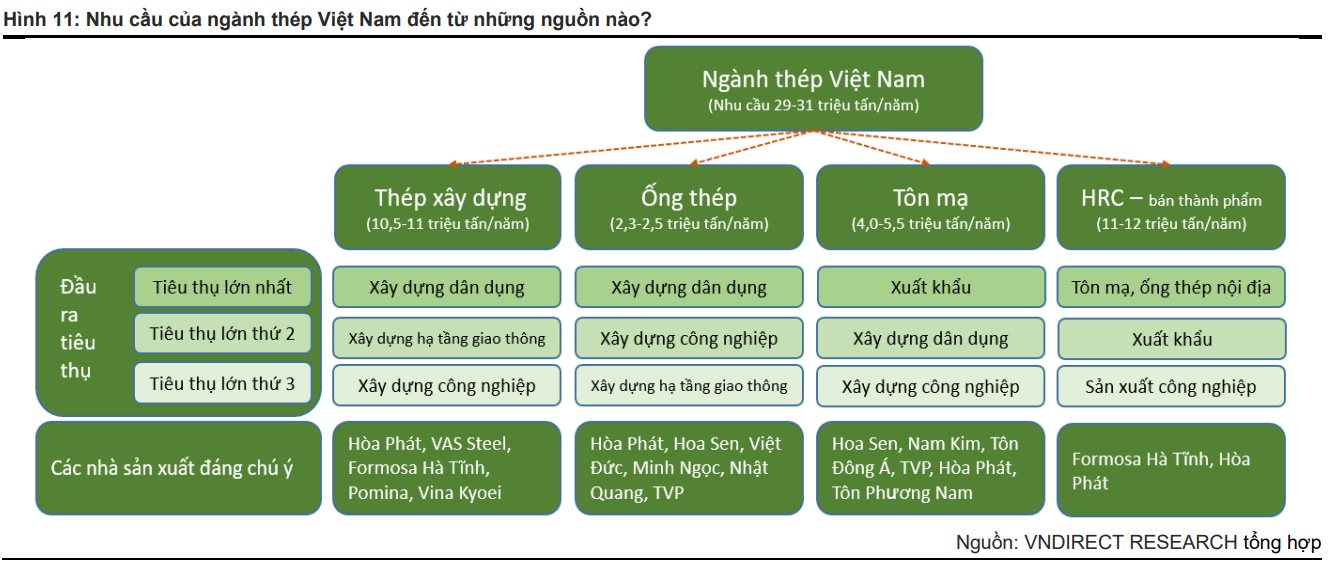

According to VNDirect Securities, the prospect of the residential real estate industry has the biggest influence on the demand for Vietnam's steel industry when accounting for about 60-65% of the industry's demand. Although the government has issued an amended Decree 10/2023/ND-CP, contributing to the settlement of legal bottlenecks, VNDirect believes that it is still too early to assess whether the real estate market will soon "defrost". when the actual effectiveness of policy implementation is still open and many bottlenecks have not been completely resolved.

VNDirect believes that policies issued to remove the real estate market from the beginning of the year can partially remove the bottleneck, but more synchronous solutions are needed in terms of both legal processes and access to capital for the real estate market. recovery real estate.

Therefore, the analysis team believes that "domestic real estate supply will only be able to recover from 2024" when (1) the revised Land Law is adopted to remove a series of legal bottlenecks and (2) ) Financial pressure, interest rates are reduced when banks create more favorable conditions to access capital as well as stimulate demand for home buyers. This leads to the fact that Vietnam's steel demand will only recover strongly from 2024.

The prolonged dismal demand of the domestic civil construction sector will have a significant impact on the demand for construction materials in 2023. Hence, although public investment disbursement is expected to accelerate in the coming years. In the next quarter, VNDirect forecasts that total domestic steel demand will grow in negative single digits in 2023.

CafeF

w300.jpg)